Table of Contents

The Tax Extension Clock is Ticking: Why You Need to Act Fast

The October 15 deadline is rapidly approaching. If you filed for an extension earlier this year, that day is the final countdown for filing your tax return. Rushing to find a year’s worth of invoices, receipts, and financial statements can lead to missed deductions, errors, and significant stress. In fact, taxpayers who file an extension often have more complex financial situations, making organization an even bigger challenge.

The stakes are high. According to the IRS, a failure to file penalty is typically 5 percent of the unpaid taxes for each month or part of a month that a return is late, with a maximum penalty of 25 percent. The best way to avoid this is to have all your records in order.

The Solution: Get Your Records in Order, Now

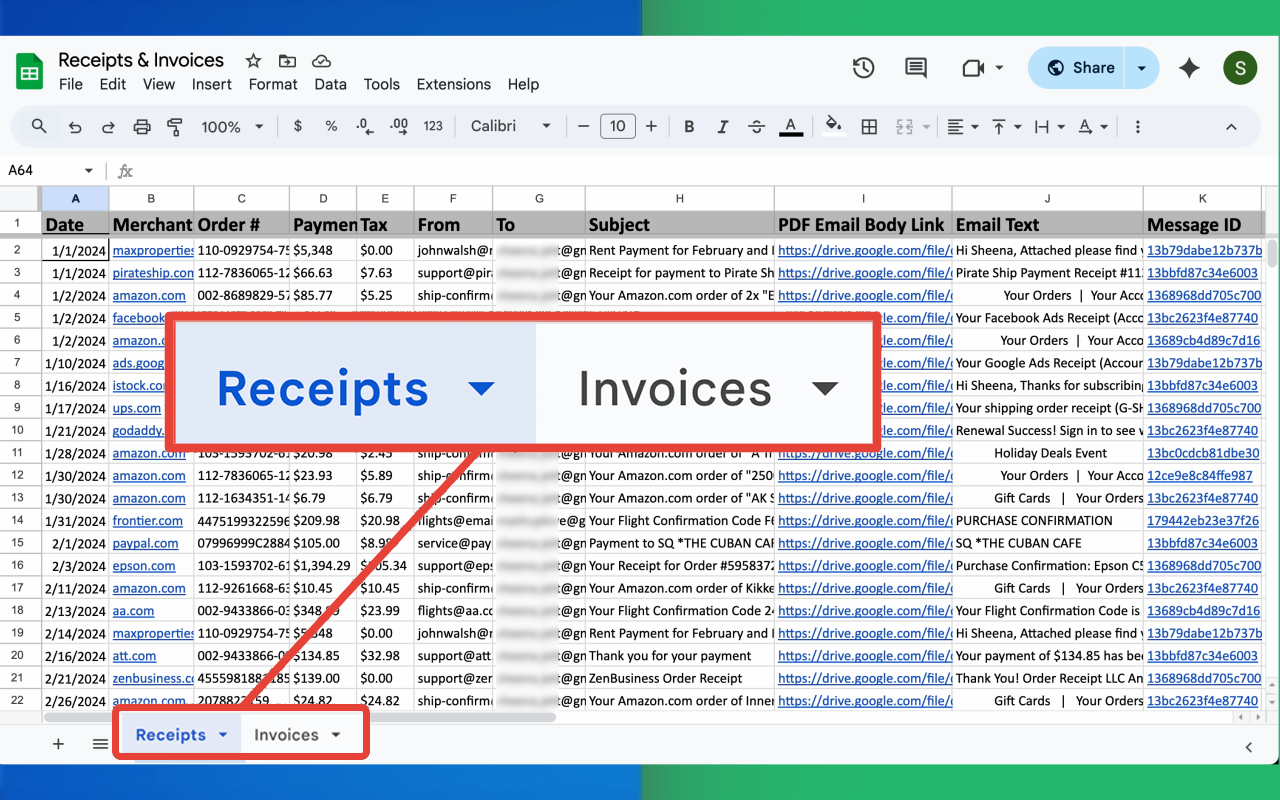

The first and most important step to putting out this tax fire is to get a handle on your records. This is where Get My Receipts comes in. It provides an immediate and efficient way to digitally capture and export all your invoices and receipts, no matter where they are. You can use this service to:

- Digitize All Documents: Quickly scan and upload paper receipts before they fade.

- Centralize Your Data: Bring together invoices from different platforms into a single, secure location.

- Export Everything: Generate comprehensive reports and exports that can be easily shared with your tax preparer.

Having a clean, categorized set of records is not just about making the filing process easier. It is a vital defense in case of an IRS audit. According to the IRS, the general statute of limitations for an audit is three years from the date you file, but this can be extended to six years if you underreport your gross income by more than 25 percent. Organized records are your primary evidence.

That’s why cloudHQ created Get My Receipts, an easy-to-use app that goes through all of your Gmail emails and extracts all your receipts and invoices to organize them in a Google Sheet spreadsheet for you to edit, share, and keep track of.

From Firefighting to Financial Freedom: The Case for Year Round Tax Planning

Once you have successfully filed your return, the October 15 deadline should be a wake up call. It is a reminder that tax management should be a continuous process, not a last minute scramble. Proactive, year round tax planning can help you maximize savings, avoid penalties, and gain financial confidence.

5 Key Tax Planning Pointers

- Check Your Withholding: Your federal income taxes are paid throughout the year. It is crucial to review your tax withholding, especially after life changes like a new job, marriage, or a new child. The IRS Withholding Tax Estimator can help ensure you are withholding the correct amount.

- Organize Tax Records: A simple and effective record keeping system is vital. Organized records make tax return preparation easier and can help you uncover overlooked deductions or credits.

- Understand Adjusted Gross Income (AGI): Your AGI is your total income minus certain adjustments. It is a key factor in determining your tax rate and eligibility for various tax benefits. Tax planning can include making changes that lower your AGI, such as contributing to a retirement account or a Health Savings Account.

- Save for Retirement: Contributions to retirement plans like a 401(k) or traditional IRA can reduce your taxable income. This is a powerful strategy for lowering your tax liability while building a nest egg for the future.

- Update Personal Information: Always notify the United States Postal Service, your employer, and the IRS of any address or legal name changes.

Leveraging Tax Deductions and Credits

Understanding the difference between tax deductions and tax credits is a crucial part of effective tax planning. A tax deduction reduces your taxable income, which in turn lowers your tax liability. A tax credit, on the other hand, provides a dollar for dollar reduction of your tax bill. Tax credits are generally more valuable than deductions.

Common Deductions and Credits

- Charitable Contributions: If you itemize your deductions, you can deduct cash or property donations to qualified organizations. According to data from the IRS, in 2022, individuals with adjusted gross income over $10 million accounted for nearly half of the total amount donated via non-cash charitable contributions. This shows the significant role philanthropy plays in high-level tax planning.

- Educational Expenses: The costs of higher education can bring significant tax benefits. The American Opportunity Tax Credit (AOTC) provides a credit of up to $2,500 per eligible student for the first four years of postsecondary education. The Lifetime Learning Credit (LLC) is a non refundable credit of up to $2,000 for courses taken to acquire or improve job skills.

- Health Savings Accounts (HSAs): Contributions to an HSA are a powerful tax tool. They are tax deductible, grow tax free, and withdrawals for qualified medical expenses are also tax free. This triple tax advantage makes an HSA a key component of financial planning for those with a high deductible health plan.

Tax Planning for the Self Employed and Small Business Owners

If you are self employed, tax planning is an even more active process than for a traditional employee. You are responsible for both the employer and employee portions of Social Security and Medicare taxes, known as self employment tax. The IRS scrutinizes self employed tax returns more closely than those of traditional wage earners, making accurate record keeping absolutely essential.

Smart Investment Strategies: The Power of Tax Loss Harvesting

Managing your investments isn’t just about growth. It is also about managing the tax consequences of that growth. Tax loss harvesting is a strategy that can help you reduce your tax liability. It involves selling investments that are performing poorly at a loss to offset capital gains from other investments you have sold at a profit. This can reduce or even eliminate the taxes you would owe on those gains. The best way to track this is with clear, digital records, which again, is where Get My Receipts can be a huge asset.

By thinking about taxes throughout the year and keeping detailed records, you are not just preparing to file. You are actively building a stronger financial future.